Monthly macro and economic insights report

By economist Dr Roelof Botha

Offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the ever-changing economic landscape.

April 2026

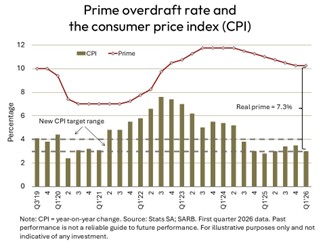

Repo rate on hold

At its March policy meeting, the Reserve Bank’s Monetary Policy Committee (MPC) decided to keep its repo rate on hold at 6.75%. This translates into a steady prime overdraft rate of 10.25% (which remains higher than the rate existing before COVID-19). The reasons behind the decision to hold the repo rate at its current level were obviously related to inflationary fears over higher fuel prices.

During the January meeting of the MPC, two of the six MPC members voted for a 25 basis point reduction of the repo rate; the other four members chose to hold the rate steady. This suggests that any swift ending to the war in the Middle East may soon lead to a further relaxation of monetary policy – a prospect that has been boosted by the recent decline in the rate of inflation.

Both the consumer price index (CPI) and the producer price index (PPI) resumed a downward trend in February, with the CPI declining from 3.5% to 3% and the PPI dropping from 2.2% to 1.8%. Inflation at the factory gate has now been below 3% for 19 successive months, and this price gauge serves as a leading indicator for consumer price trends. Although the spike in fuel prices will inevitably filter through to broad-based inflationary pressures, the current low base of inflation provides the MPC with substantial breathing space to keep the lending rate steady.

Solid trade balance performance

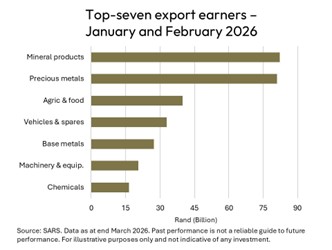

South Africa’s international trade account has started 2026 on a high note, mainly as a result of lower imports and the record prices for gold and platinum. Despite only half of the top 10 export sections recording a trade surplus during the first two months of the year, the 39% year-on-year increase in the value of precious metal exports played a key role in securing a healthy cumulative trade surplus of R45.4 billion. (This figure dwarfs the meagre R3.3 billion surplus recorded in January and February last year.)

The top three contributors to the cumulative trade surplus during January and February were the sections for precious metals, minerals, and agriculture & food – contributing 62.8% tot total exports. Agriculture & food has now leapfrogged the section for vehicles & spares to assume the position as the third most important foreign exchange earner via goods exports.

With the rand exchange rate taking a knock in the wake of the Middle East war, the chances for higher future export earnings in rand terms have improved, whilst the stronger currency is also likely to lead to some discouragement of imports. The only red flag is the spike in the oil price, which has already resulted in fuel price increases and will inevitably lead to a higher value for mineral imports during the second quarter of the year.

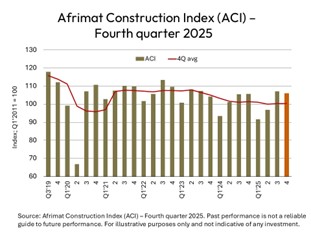

Building materials boost construction sector

The Afrimat Construction Index (ACI) for the fourth quarter of 2025 shows a marginal year-on-year increase, boosted by a 5.4% increase in the volume of building materials produced and a 2.2% real increase in the sales value of building materials. These two indicators carry the largest weighting in the composite index of the level of construction activity in South Africa.

Although the activity levels in South Africa’s construction sector remain subdued, the ACI’s seasonally adjusted reading has increased for the second consecutive quarter (the first time this has occurred since the brief recession of 2020). Five of the 10 indicators recorded positive year-on-year growth rates, whilst seven of them managed positive quarter-onquarter growth during the fourth quarter of 2025. According to Afrimat, the rate-cutting cycle of the monetary policy authorities has played a crucial role in lowering the cost of capital formation, which invariably involves construction works and building activity.

An exceptionally strong performance of private sector capital formation in buildings and construction works has been observed since interest rates were lowered from a 15-year high towards the end of 2024. It is also encouraging that the National Treasury has set aside an amount of R141 billion for water resources and road infrastructure in the current fiscal year. Hopefully, the private sector will also become more involved in the early stages of such projects, including technical tender specifications, evaluation and, ultimately, also monitoring and evaluation.

About Dr Roelof Botha

A seasoned veteran of the economics fraternity in South Africa, Dr Botha has more than 50 years’ experience as a lecturer, financial editor of a daily newspaper, economic policy advisor at the National Treasury, columnist for various publications, researcher and a public speaker. Dr Botha received his early schooling in Sweden, Germany, The Netherlands, Christiana in the North West Province, as well as in Cape Town and Pretoria. His postgraduate qualifications include Honours and master’s degrees in economics (cum laude) at the University of Pretoria, and a Doctorate at the University of Johannesburg. He has authored more than 2000 articles, research papers and books, and has received the prestigious Finmedia Economist of the Year award, based on the accuracy of forecasts of key economic indicators.

Dr Botha teaches economics (part-time) at the Gordon Institute of Business Science (GIBS) and is the Economic Advisor to the Optimum Financial Services Group.

Disclaimer

Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, Optimum Investment Group (OIG) does not accept any responsibility for any claim, damages, loss or expense, however, it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary.

Optimum Investment Group (Pty) Ltd. Is an Authorised Financial Services Provider (43488).

All investments involve risk, including the potential loss of principal. There is no assurance that any financial strategy will be successful. OIG does not guarantee that the results of any advice, recommendations, or strategies will be achieved. Before making any investment decisions, customers should thoroughly review all relevant investment product documents and information. It is essential to assess whether an investment aligns with your financial situation, objectives, and risk profile.

This document may contain forward-looking statements identified by terms such as “expects,” “anticipates,” “believes,” “estimates,” “forecasts,” and similar expressions. These statements involve risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. OIG is not responsible for any trading decisions, damages, or other losses resulting from the use of the information, data, analyses, or opinions provided.

Past performance does not guarantee future results. Neither diversification nor asset allocation ensures a profit or protects against a loss.

The information, data, analyses, and opinions presented herein are for informational purposes only and do not constitute investment advice or an offer to buy or sell any security. References to specific securities or investment options should not be considered an offer to purchase or sell those investments. The performance data shown reflects past performance and is not indicative of future results.

The opinions expressed are those of OIG as of the date written, are subject to change without notice, and do not constitute investment advice.