Our monthly To the Point column by economist Dr Roelof Botha offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the everchanging economic landscape

MONTHLY MACRO AND ECONOMIC INSIGHTS REPORT

December 2025

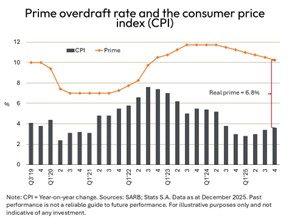

Welcome relief for borrowers

During November, the Monetary Policy Committee (MPC) of the Reserve Bank continued its rate-cutting cycle that commenced 14 months ago. This resulted in a prime overdraft rate of 10.25%, compared to 11.75% at the beginning of September last year.

The move was widely welcomed and even prompted a media statement from the national government, stating that a lower interest rate provides much-needed relief for South African households, many of whom continue to face financial pressure due to the rising cost of living.

The current prime rate remains higher than just before the COVID-19 lockdowns were implemented in 2020. Additionally, it remains 325 basis points higher than the rate that prevailed in October 2021. It is clear from the lethargic growth in household disposable income and the high level of unutilised capacity in the manufacturing sectors that demand-side inflation is absent from the South African economy. A further lowering of interest rates is bound to stimulate demand and also output, which will assist in lowering the country’s unemployment rate.

Unfortunately, the prospect for further rate cuts has been dampened by the recent rise in the consumer price index (CPI), which is now within touching distance of the upper level of the implicit new inflation target range. The Minister of Finance, on 12 November 2025, announced a new inflation target for South Africa of 3% with a 1 percentage point tolerance band. Any significant depreciation of the rand exchange rate is therefore destined to halt the modestly more accommodating policy stance of the MPC.

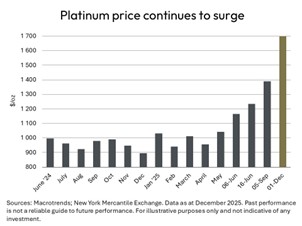

Precious metals remain in demand

The surge in the price of gold and platinum during 2025 is exceptionally good news for South Africa. Gold leads the way with an all-time high recorded during October. Although it has retraced somewhat since then, gold was trading at $4,257 per fine ounce on 1 December.

The most recent rise has been attributed to a strong likelihood of further interest rate cuts in the US, as well as changes to the leadership at the country’s central bank, the Federal Reserve.

After taking a dip to just below $1,500 per fine ounce on 21 November, platinum bounced back to reach a level of $1,700 on 1 December – its highest price in 12 years.

According to the World Platinum Investment Council, demand for platinum jewellery is projected to rise 7% during 2025 (year-on-year) to its highest level since 2018, propelled by growth across most global markets. Platinum jewellery is reaping the benefits from the high gold price by virtue of its relative price discount.

The Resource-10 index on the JSE has received an extraordinary boost from the splendid rise in precious metal prices, gaining 131% between the end of last year and 1 December 2025. In comparison, the all-share index (ALSI) increased 32% over the same period. No doubt National Treasury will witness a handsome overrun on its revenue budget from company tax for 2025/26. Another positive spin-off is the year-on-year increase of 13% in export earnings by the precious metals section between January and October 2025.

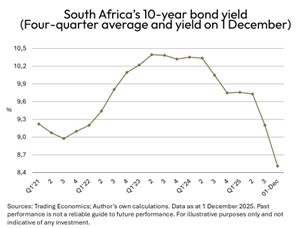

Sharp decline in 10-year bond yield

South Africa’s benchmark long-term interest rate, the 10year government bond yield, has declined by 260 basis points since early April. On 1 December, the yield stood at 8.52% – its lowest level since February 2021, signalling a welcome decline in the borrowing costs associated with public debt denominated in foreign currencies. The decline in the benchmark short-term interest rate since September last year is 150 basis points – suggesting ample scope for a further easing of the Reserve Bank’s repo rate.

Reasons for the lower bond yield include the modest relaxation of monetary policy by the Reserve Bank, lower domestic inflation and South Africa’s recent removal from the so-called ‘grey list’ of the Financial Action Task Force. Furthermore, fiscal conditions have improved, with sound prospects for a second successive primary budget surplus (tax revenue minus non-interest government expenditure).

The recent decline in the yield on US treasuries, as well as the US dollar index (also referred to as the ‘Dixie’), has also played their part, with an increased appetite for investment in emerging market and developing economies (EMDEs) having come to the fore amongst global fund managers.

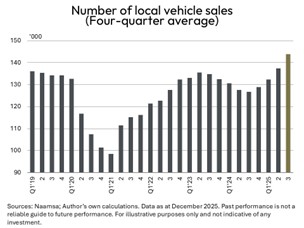

New record number of vehicle sales

During the third quarter of 2025, the number of vehicle sales in South Africa increased by 20% (year-on-year) and by 17% (quarter-on-quarter) to reach a record high of more than 52,000 units. The figure shows the sharp decline in vehicle sales during the worst of the Covid-19 pandemic, followed by a remarkably swift recovery to virtually the same level as prior to Covid-19, mainly as a result of pent-up demand and the fact that the prime rate was lowered from 10% to 7%.

The Monetary Policy Committee (MPC) of the Reserve Bank then went on a rate-hiking spree that ultimately resulted in an increase of 68% in the cost of credit (as measured by the prime rate), which predictably resulted in another downward trend in the number of new vehicle sales. Fortunately, the positive impact of the subsequent lowering of the prime rate (via the repo rate) has now resulted in a new record high for this indicator. This was also reflected in the Drive.co.za Motor Index (DMI), which has reached its highest level since the base period of 2018.

Another positive feature of the latest data underpinning the DMI is the new record high for the real value of exports of vehicles and components during the third quarter of 2025. This has occurred despite the uncertainty surrounding the higher tariffs imposed on many of South Africa’s exports to the US and the relatively slow transition to electric vehicle manufacturing in South Africa (including hybrids). The section for exports of vehicles and components remains the third largest contributor to South Africa’s goods export earnings.

About Dr Roelof Botha

A seasoned veteran of the economics fraternity in South Africa, Dr Botha has more than 50 years’ experience as a lecturer, financial editor of a daily newspaper, economic policy advisor at the National Treasury, columnist for various publications, researcher and a public speaker. Dr Botha received his early schooling in Sweden, Germany, The Netherlands, Christiana in the North West Province, as well as in Cape Town and Pretoria. His postgraduate qualifications include Honours and Master’s degrees in economics (cum laude) at the University of Pretoria, and a Doctorate at the University of Johannesburg. He has authored more than 2000 articles, research papers and books, and has received the prestigious Finmedia Economist of the Year award, based on the accuracy of forecasts of key economic indicators.

Dr Botha teaches economics (part-time) at the Gordon Institute of Business Science (GIBS) and is the Economic Advisor to the Optimum Financial Services Group.

Disclaimer

Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, Optimum Investment Group (OIG) does not accept any responsibility for any claim, damages, loss or expense, however, it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary.

Optimum Investment Group (Pty) Ltd. Is an Authorised Financial Services Provider (43488).

All investments involve risk, including the potential loss of principal. There is no assurance that any financial strategy will be successful. OIG does not guarantee that the results of any advice, recommendations, or strategies will be achieved. Before making any investment decisions, customers should thoroughly review all relevant investment product documents and information. It is essential to assess whether an investment aligns with your financial situation, objectives, and risk profile.

This document may contain forward-looking statements identified by terms such as “expects,” “anticipates,” “believes,” “estimates,” “forecasts,” and similar expressions. These statements involve risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. OIG is not responsible for any trading decisions, damages, or other losses resulting from the use of the information, data, analyses, or opinions provided. Past performance does not guarantee future results. Neither diversification nor asset allocation ensures a profit or protects against a loss. The information, data, analyses, and opinions presented herein are for informational purposes only and do not constitute investment advice or an offer to buy or sell any security. References to specific securities or investment options should not be considered an offer to purchase or sell those investments. The performance data shown reflects past performance and is not indicative of future results. The opinions expressed are those of OIG as of the date written, are subject to change without notice, and do not constitute investment advice.