AS Sure Investment Services, in collaboration with Optimum Investment Group, enable our clients to have access to a well-versed investment team with extensive experience in both local and global asset management, which allows clients to grow their wealth and meet their investment objectives. This document outlines financial market movements as well as the effects it had on the AS Forum Funds.

December 2025

Global markets were relatively flat in November as investors worried about high technology valuations. The MSCI World Index rose just 0.3% but remains up 20.6% for the year. In contrast, the JSE continued its winning streak with a ninth consecutive monthly gain of 1.7%, pushing the All-Share Index past 115,000 points for the first time and bringing year-to-date returns to 31.9%.

LOCAL MARKETS

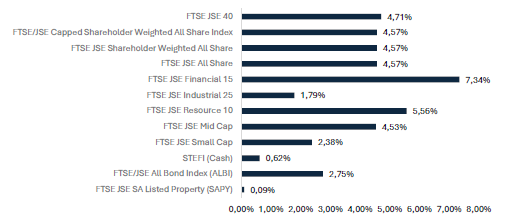

Exhibit 1 | Local Performance (ZAR) for December 2025

Source: Factset. Data as at 31 December 2025. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

South Africa

Economy

South Africa’s macroeconomic backdrop continued to improve into year-end, providing a supportive foundation for local financial assets. Headline consumer inflation slowed to 3.5% year-on-year in November, down from 3.6% in October. Core inflation edged slightly higher to 3.2% year-on-year, reflecting lingering services price pressures.

External balances strengthened meaningfully, with South Africa recording a preliminary trade surplus of R37.7 billion in November, more than double October’s R15.0 billion surplus. This marked the largest monthly trade surplus of 2025, supported by resilient commodity exports and softer import demand. Improved trade dynamics, combined with favourable global risk sentiment, contributed to sustained support for the rand.

Equity Markets

The South African equity market extended its strong run in December, recording a tenth consecutive monthly gain. The FTSE/JSE All Share Index rose 4.6% during the month, lifting its full-year return to 42.4%, the strongest annual performance in nearly two decades. In US dollar terms, the JSE also ranked among the top-performing global equity markets for 2025.

Precious metal miners remained the dominant driver of local equity performance. A powerful rally in gold and platinum prices provided a significant boost to commodity-linked shares, with the Resources 10 Index gaining 5.6% in December and more than 144% over the year.

Financial shares also contributed positively in December, with the Financial 15 Index rising 7.3% as improving sentiment toward South Africa’s economic outlook supported banks and insurers. Industrials delivered modest gains, while listed property delivered 0.1% during the month; the sector ended 2025 with a solid 30.6% in returns.

Best performers:

Implats 22.20%

Valterra Platinum Ltd 18.41%

Absa Group 14.92%

Glencore Plc 11.74%

Firstrand 11.39%

Worst performers:

Mr Price Group 15.15%

Sasol 4.58%

British American Tobacco 3.87%

Prosus 3.70%

Clicks Group – 3.06%

Bond Market:

South African bonds ended the year strongly. The government’s 10-year borrowing rate declined further to 8.2%, its lowest level in more than a decade, having fallen by over 200 basis points during 2025. As a result, the FTSE/JSE All Bond Index returned 2.8% in December and an impressive 24.2% for the year.

The rand was a standout performer in December, appreciating 3.3% against the US dollar. This capped off a strong year for the local currency, which strengthened by 13.8% over 2025, ending the year at R16.56/USD. The rally was supported by a weaker US dollar, strong capital inflows, and South Africa’s improving terms of trade.

GLOBAL MARKETS

Global equity markets ended 2025 with modest gains in December, although performance varied significantly by region. Developed market equities rose 1.1% for the month, taking full-year returns to 22.9% and marking a third consecutive year of strong global equity performance.

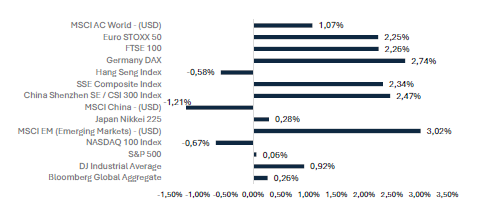

Exhibit 2 | Global Performance (base currency) December 2025

Source: Factset. Data as at 31 December 2025. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

US equities underperformed their global peers into year-end. The S&P 500 Index edged up just 0.1% in December, while the Nasdaq 100 declined 0.7% as concerns grew around the scale of artificial intelligence-related capital expenditure and its ability to translate into sustained earnings growth. Several mega-cap technology stocks experienced sharp share price declines following earnings updates that highlighted rising investment costs and more cautious revenue outlooks. Despite this, US equities still delivered solid returns for the year, with the Nasdaq 100 ending 2025 up 21%.

On the policy front, the US Federal Reserve delivered its third consecutive 25-basis-point rate cut at its December meeting. The decision was notable for the unusually high number of dissenting votes, underscoring the tension between supporting a weakening labour market and containing persistent inflation pressures. The US 10-year government bond yield ended the year at 4.2%.

Europe

European equity markets delivered a strong performance in December, extending an already robust year for the region. The Euro Stoxx 50 Index gained 2.3% month-on-month in December, supported by broad-based strength across financials, industrials, and select consumer sectors. Investor sentiment continued to improve as easing financial conditions, falling bond yields, and supportive fiscal measures in key economies underpinned equity valuations.

Germany’s DAX was a standout performer, rising 2.7% in December, buoyed by government-led fiscal support initiatives and targeted infrastructure spending aimed at stimulating domestic growth. For the full year, European equities recorded their strongest annual performance since 2021, reflecting both cyclical recovery dynamics and a rotation toward more attractively valued markets within developed economies.

United Kingdom

In the United Kingdom, the FTSE 100 gained 2.7% in December, supported by strength in energy and financial stocks. Oil majors benefited from resilient commodity prices, while banks were underpinned by stable net interest margins. UK inflation remained elevated at 3.8% year-on-year for a third consecutive month, reinforcing expectations that the Bank of England will maintain a cautious approach to monetary easing in early 2026.

Asia

Asian markets delivered mixed performances. Japan’s Nikkei ended December slightly higher at 0.3%, supported by easing inflation pressures and continued optimism around economic policy. In China, equity markets remained under pressure, reflecting weak domestic demand and ongoing structural challenges. However, economic data showed tentative signs of stabilisation, with manufacturing activity returning to expansion territory for the first time since March.

Emerging Markets

Emerging market equities outperformed developed markets in December. The MSCI Emerging Markets Index gained 3% for the month and ended 2025 ahead of developed markets for the first time since 2020. Performance was driven largely by technology-heavy Asian markets, particularly semiconductor manufacturers, which benefited from sustained global demand linked to AI investment.

Commodities and currencies

In December 2025, commodities showed a mixed performance, with energy prices declining while precious and industrial metals surged. Brent crude fell 3.7% in December to US$60.85/bbl amid expectations of oversupply. In contrast, precious metals experienced strong gains, with gold up 1.9% in December, platinum soaring 23.3%, palladium rising 11.4%, and rhodium climbing 15.0%, driven by safe-haven demand, expectations of further US rate cuts, elevated geopolitical risk, and central bank buying. Iron ore also advanced 2.6% in December, supported by robust Chinese demand, strong steel exports, and improving steel market fundamentals.

The US dollar weakened in December, with the US Dollar Index falling 1.1% and ending the year down 9.4%, its worst annual performance in nearly a decade. The softer dollar provided support to emerging market currencies and commodity prices into year-end.

Outlook

December capped off an exceptional year for South African assets, with equities, bonds, and the rand all delivering strong real returns. The continued dominance of precious metal miners highlights the importance of commodity exposure in the local market, while the late-year recovery in domestic sectors suggests improving confidence in South Africa’s economic outlook.

Globally, market leadership is broadening beyond US mega-cap technology stocks, with Europe and emerging markets increasingly attracting investor attention. While monetary easing and resilient growth continue to support risk assets, elevated valuations, geopolitical uncertainty, and policy divergence remain key risks.

As markets enter 2026, disciplined diversification and selective positioning will be critical as investors navigate an environment characterised by slowing growth, shifting rate expectations, and evolving regional opportunity Performance Review | December 2025

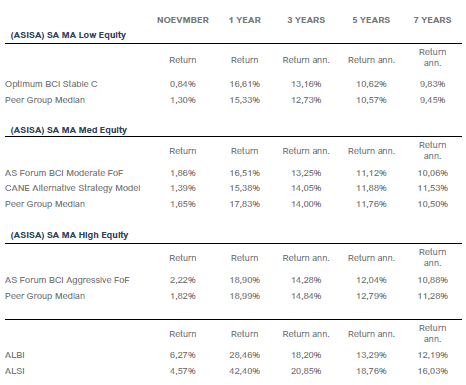

Source: OIG, FundFocus. Data as at 30 November 2025. Past performance is not indicative of future performance.

Disclaimer

Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, Optimum Investment Group (OIG) does not accept any responsibility for any claim, damages, loss or expense, however, it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary.

Optimum Investment Group (Pty) Ltd. Is an Authorised Financial Services Provider (43488).

All investments involve risk, including the potential loss of principal. There is no assurance that any financial strategy will be successful. OIG does not guarantee that the results of any advice, recommendations, or strategies will be achieved. Before making any investment decisions, customers should thoroughly review all relevant investment product documents and information. It is essential to assess whether an investment aligns with your financial situation, objectives, and risk profile.

This document may contain forward-looking statements identified by terms such as “expects,” “anticipates,” “believes,” “estimates,” “forecasts,” and similar expressions. These statements involve risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. OIG is not responsible for any trading decisions, damages, or other losses resulting from the use of the information, data, analyses, or opinions provided. Past performance does not guarantee future results. Neither diversification nor asset allocation ensures a profit or protects against a loss. The information, data, analyses, and opinions presented herein are for informational purposes only and do not constitute investment advice or an offer to buy or sell any security. References to specific securities or investment options should not be considered an offer to purchase or sell those investments. The performance data shown reflects past performance and is not indicative of future results. The opinions expressed are those of OIG as of the date written, are subject to change without notice, and do not constitute investment advice.