Monthly macro and economic insights report

Our monthly To the Point column by economist Dr Roelof Botha offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the ever-changing economic landscape.

February 2026

Rand ends 2025 on a high note

The gold price has been acting like a runaway train and is probably in line for a nomination as business newsmaker of the year. On January 28, the gold price reached a new all-time high of more than $5,200 per fine ounce, before retreating to just below $5,000 by month-end.

The gold price has been acting like a runaway train and is probably in line for a nomination as business newsmaker of the year. On January 28, the gold price reached a new all-time high of more than $5,200 per fine ounce, before retreating to just below $5,000 by month-end.

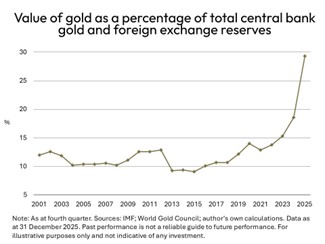

One of the interesting features of the spectacular rise in the gold price since the beginning of 2024 is the profound shift in the valuation of foreign exchange reserves by the world’s central banks. In 2000, the gold component of these reserves represented 14% of the total, with the bulk of central bank reserves being vested in US treasuries, followed by Euro bonds.

This ratio followed a fairly modest growth path over the first quarter of the 21st millennium to reach a level of 20% but has now exploded to reach a new record high of just below 30%. According to the World Gold Council, central banks have been shoring up the gold component of their official reserves, especially due to recent declines in US interest rates and heightened geopolitical uncertainty. At the current price, however, the opportunity cost of swapping interest-bearing bonds for physical gold has become very high.

All of this is exceptionally good news for South Africa, as gold continues to play a key role in the country’s mining sector, providing jobs to 450,000 people. According to the latest US Geological Survey, South Africa is ranked third in the world for unmined gold reserves, behind Australia and Russia. With the price of the world’s premier precious metal at record highs, the chances of higher mining sector profits should also assist the National Treasury’s task of maintaining fiscal stability.

Retail sales bonanza in November

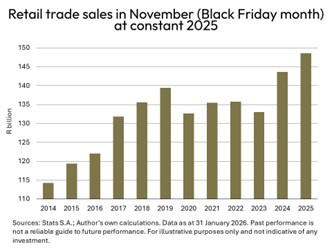

The reduction in the cost of credit during 2025 was always going to lead to a stronger growth momentum for retail trade sales, and South African shoppers did not disappoint the forecasters. November witnessed retail trade sales of R148 billion – a new record and 3.5% higher than the figure for 2024 (in real terms).

By virtue of the Black Friday phenomenon and the Christmas festive season, the fourth quarter of every year has a long-standing tradition as the best turnover period for retailers.

The sectors that fared the best during 2025 were pharmaceuticals, furniture & appliances and the category for “other”, which mainly includes books, stationery, jewellery, watches and sports equipment, all of which managed to beat inflation by a healthy margin.

The sectors that fared the best during 2025 were pharmaceuticals, furniture & appliances and the category for “other”, which mainly includes books, stationery, jewellery, watches and sports equipment, all of which managed to beat inflation by a healthy margin.

An interesting feature of South Africa’s retail trade sales is the rapid growth of online spending. According to the Retail Spend Monitor from Visa Consulting and Analytics, e-commerce continues to expand in South Africa as online retail spending increased by 50% in 2025 to reach a level of 11.5% of total retail sales. The latter figure is slightly higher than the 10% quoted by the E-commerce Forum South Africa (EFSA) but still significantly lower than the global average of above 20%, as surveyed by eMarketer.

Apart from the welcome decline in interest rates during 2025, retail trade sales have also been driven by modest increases in employment and average salaries, early-season promotions and a strong focus on discounts. Online shopping has benefited from a combination of convenience, an expanding base of suppliers and AI-related personalisation.

Trade surplus hits R200 billion in 2025

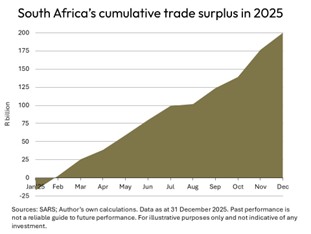

Following the traditional modest trade deficit during the first month of each year, the value of South Africa’s exports started to outstrip the value of imports during 2025 to ultimately produce a cumulative trade surplus of exactly R200 billion. Last year was the fourth year in succession that total exports managed to breach the R2-trillion level.

Following the traditional modest trade deficit during the first month of each year, the value of South Africa’s exports started to outstrip the value of imports during 2025 to ultimately produce a cumulative trade surplus of exactly R200 billion. Last year was the fourth year in succession that total exports managed to breach the R2-trillion level.

From the perspective of the different export sections, the turbulent international trading environment (caused by the so-called tariff wars) has resulted in mediocre growth for the exports of chemicals, pulp and machinery and equipment, whilst 2025 witnessed declines in the export values of base metals and mineral products.

Last year’s outstanding export performers were precious metals, agriculture and processed food. One of the features of South Africa’s international trade is the undue reliance on only five key product groups, viz minerals, precious metals, vehicles and spares, agriculture and food and base metals. In combination, these groups represent 80% of the country’s total foreign exchange earnings from goods exports.

Viewed from the perspective of the destination of exports of high-value-added (HVA) goods (which excludes metals and minerals), the US has dropped from the second position to number four. Belgium has climbed up the rankings to position number three. Germany remains comfortably in first place.

The Southern African Development Community continues to play a dominant role as a destination for exports of high-value-added goods, with no less than five of its member countries represented in the top ten export destinations for HVA goods. Interestingly, China is in the eleventh spot, with the United Arab Emirates and Spain having climbed up the ranks in recent years to numbers twelve and fourteenth, respectively.

House prices recover

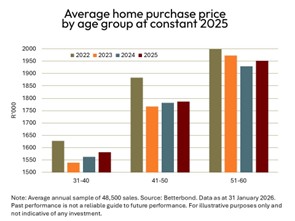

Following a marginal decline during 2024 in the residential property price index (RPPI) published by Statistics SA, average house prices started to pick up again in 2025. This is mainly due to lower interest rates, which have served to enhance the affordability of mortgage loan repayments. This trend is also evident in data published by BetterBond, South Africa’s largest mortgage bond originator, which shows a turnaround in average real home prices during 2025.

Following a marginal decline during 2024 in the residential property price index (RPPI) published by Statistics SA, average house prices started to pick up again in 2025. This is mainly due to lower interest rates, which have served to enhance the affordability of mortgage loan repayments. This trend is also evident in data published by BetterBond, South Africa’s largest mortgage bond originator, which shows a turnaround in average real home prices during 2025.

The recovery of the residential property market remains incomplete, as confirmed by the fact that the BetterBond Index of Home Loan Applications at the end of last year was still 23% down on the reading for the third quarter of 2023, when the prime overdraft rate had risen to a 15year high.

Ever since the Reserve Bank started with a rate-cutting cycle during the third quarter of 2024, house prices started to recover, although the recovery of prices for first-time home buyers has been more muted. When viewed against the background of the significant decline in the number of new houses that have been built over the past five years, it seems likely that average home prices will continue to increase in 2026. Any further lowering of interest rates will reinforce the recovery of the residential property market.

During 2025, new record highs for average house prices paid by first-time buyers and all buyers were recorded for mortgage bonds administered by BetterBond, namely R1.3 million and R1.6 million, respectively. The Western Cape continues to outperform all other regions for the average value of homes sold. At a level of R2.1 million, the average house price in the Western Cape was 40% higher than the national average.

About Dr Roelof Botha

A seasoned veteran of the economics fraternity in South Africa, Dr Botha has more than 50 years’ experience as a lecturer, financial editor of a daily newspaper, economic policy advisor at the National Treasury, columnist for various publications, researcher and a public speaker. Dr Botha received his early schooling in Sweden, Germany, The Netherlands, Christiana in the North West Province, as well as in Cape Town and Pretoria. Shorten with AI

His post-graduate qualifications include Honours and master’s degrees in economics (cum laude) at the University of Pretoria, and a Doctorate at the University of Johannesburg. He has authored more than 2000 articles, research papers and books, and has received the prestigious Finmedia Economist of the Year award, based on the accuracy of forecasts of key economic indicators.Shorten with AI

Dr Botha teaches economics (part-time) at the Gordon Institute of Business Science (GIBS) and is the Economic Advisor to the Optimum Financial Services Group.

Disclaimer

Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, Optimum Investment Group (OIG) does not accept any responsibility for any claim, damages, loss or expense, however, it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary.

Optimum Investment Group (Pty) Ltd. Is an Authorised Financial Services Provider (43488).

All investments involve risk, including the potential loss of principal. There is no assurance that any financial strategy will be successful. OIG does not guarantee that the results of any advice, recommendations, or strategies will be achieved. Before making any investment decisions, customers should thoroughly review all relevant investment product documents and information. It is essential to assess whether an investment aligns with your financial situation, objectives, and risk profile.

This document may contain forward-looking statements identified by terms such as “expects,” “anticipates,” “believes,” “estimates,” “forecasts,” and similar expressions. These statements involve risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. OIG is not responsible for any trading decisions, damages, or other losses resulting from the use of the information, data, analyses, or opinions provided.

Past performance does not guarantee future results. Neither diversification nor asset allocation ensures a profit or protects against a loss.

The information, data, analyses, and opinions presented herein are for informational purposes only and do not constitute investment advice or an offer to buy or sell any security. References to specific securities or investment options should not be considered an offer to purchase or sell those investments. The performance data shown reflects past performance and is not indicative of future results.

The opinions expressed are those of OIG as of the date written, are subject to change without notice, and do not constitute investment advice.